Health insurers' capital volume grew by EUR 13 billion in 2024

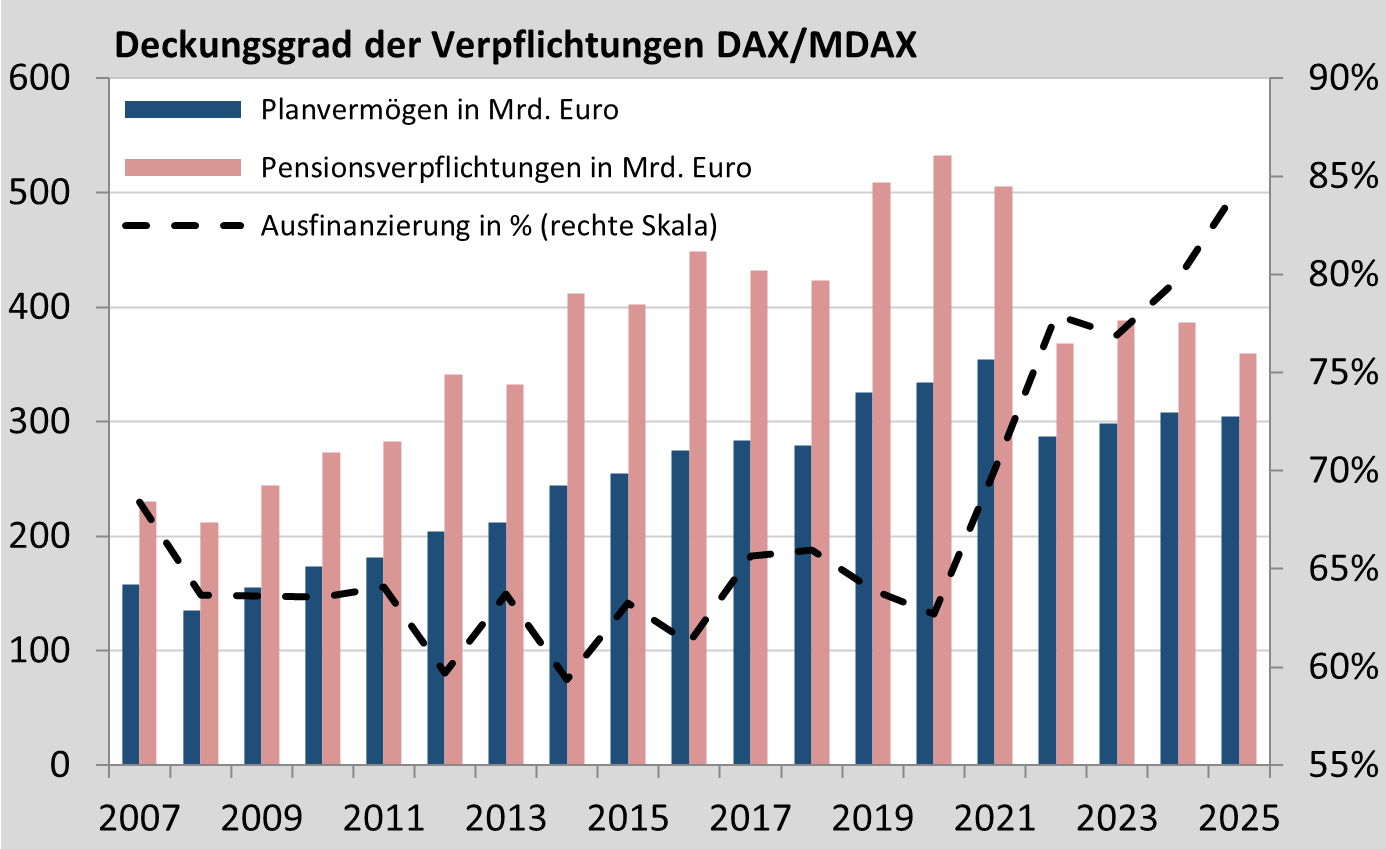

DAX/MDAX companies with record coverage ratio

Versorgungswerke: More bonds and alternatives, less equities and real estate

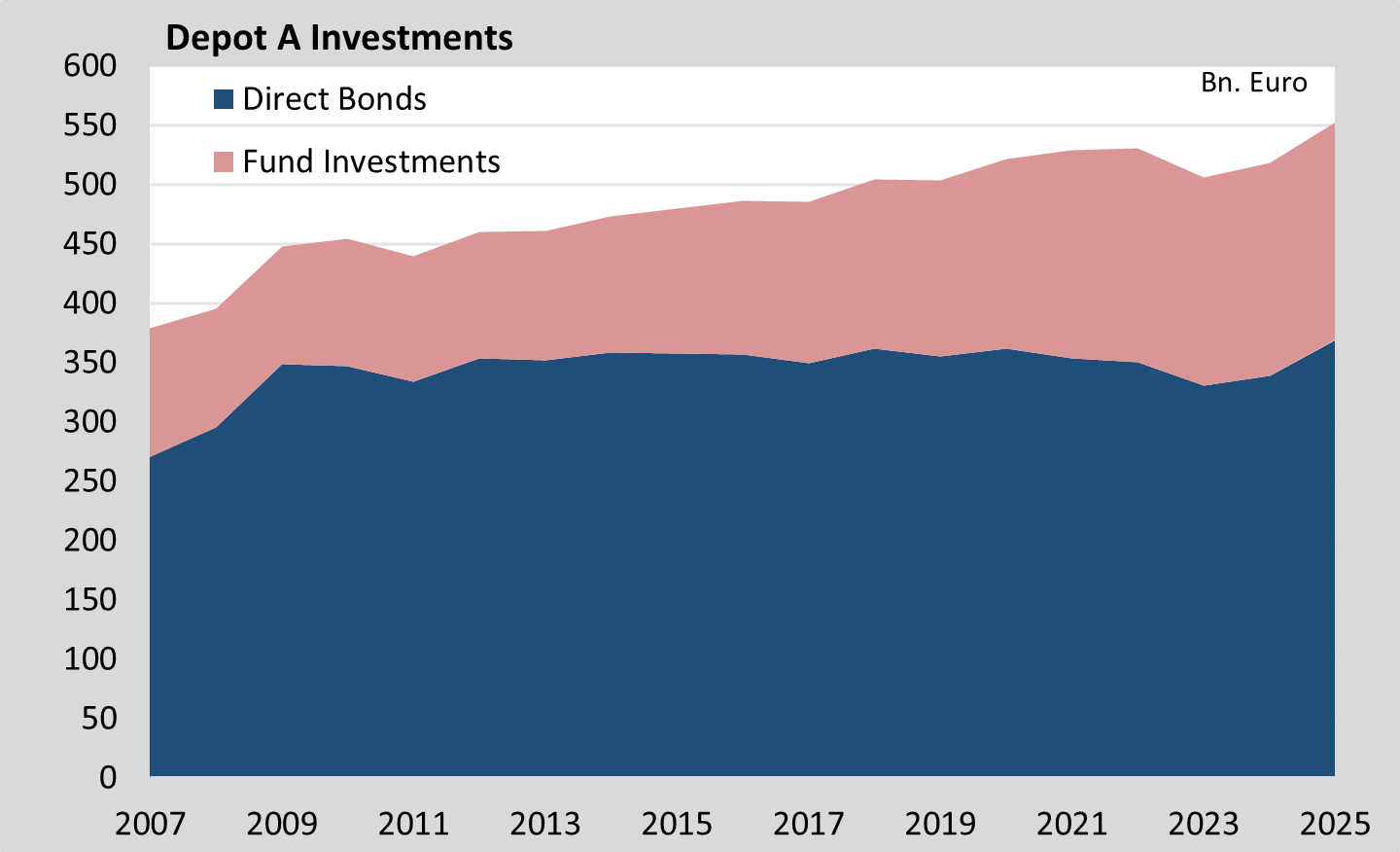

Savings Banks Depot A: Interest Income is back

Company Pension Funds 2023: Performance 6%, decreasing equity allocation

Health insurance companies: Investments increase by 4% to 360 billion euros

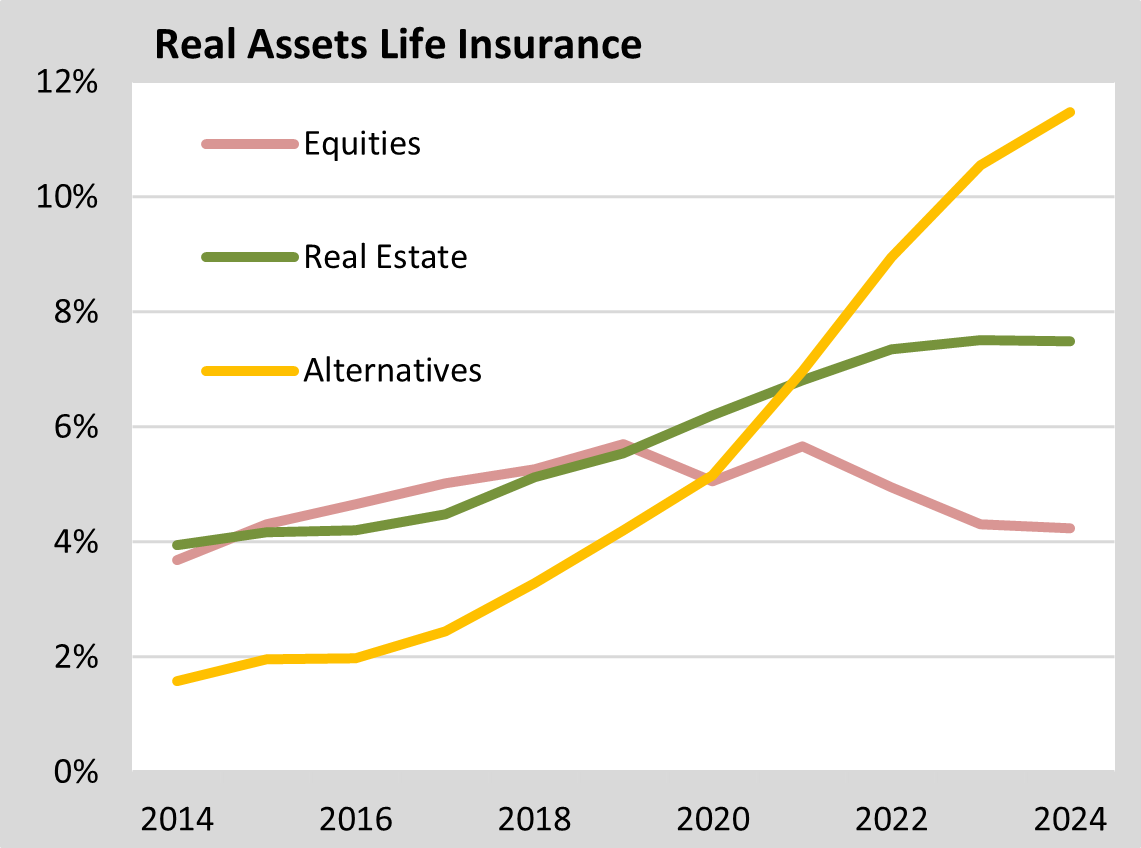

Life Insurances 2023 - Performance of around six percent

Run Off - Significant shift in allocation ratios

Obligations rise faster than plan assets in 2023 as interest rates fall

Versorgungswerke - 270 billion euros with more than 40% real estate/alternatives

Pension funds are once again focusing more on direct bond investments

Life Insurance Companies: A quarter of a trillion less

KVU: Decreasing bond and equity quota

Highly dispersed investment results 2022

CH: More than 1,000 pension funds manage over one trillion CHF

Corporates: Coverage ratio rises despite lower investment return than in 2008

Volume of Depot A securities remains at 530 billion euros in 2022

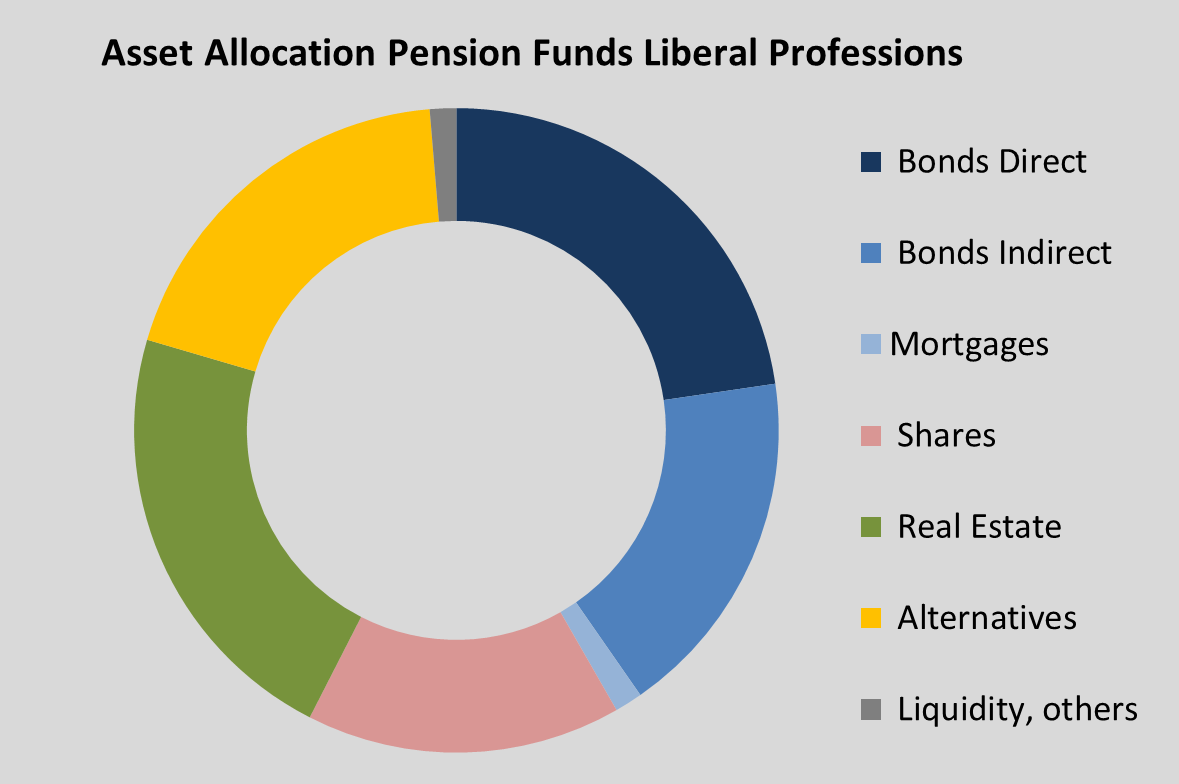

Pension funds for liberal professions with 4% net return and almost 40% illiquid assets

Pension funds continue to grow strongly

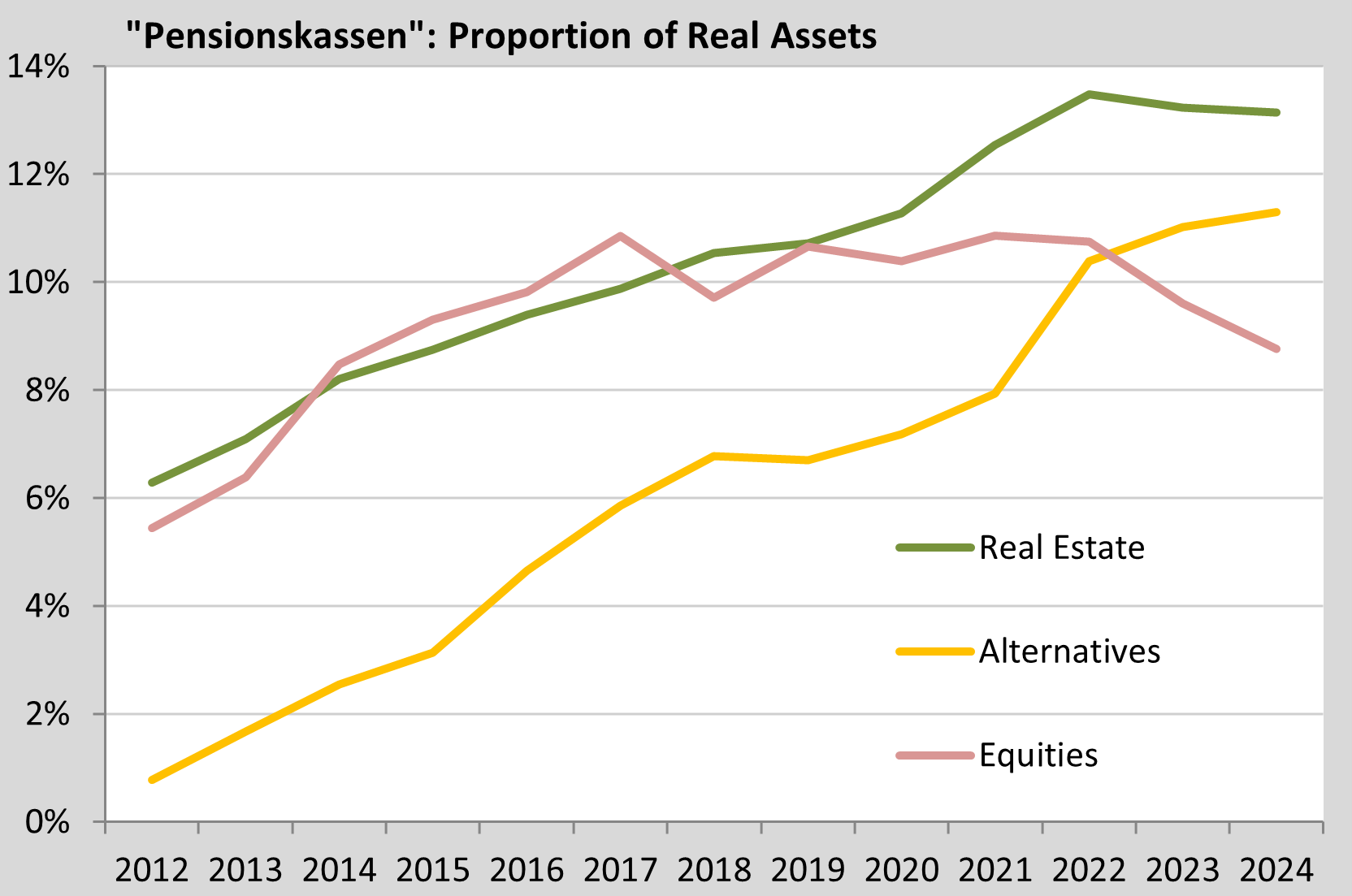

Pensionskassen - Investment volume grows by more than eight billion euros

LVU 2021 with negative market value yield, AA slowly becomes more colorful

380 billion euros with increasingly shares, real estate and alternatives

Corporates - Coverage ratio increases significantly

Depot A - Funds volume at record level

Pension Funds for liberal Professions: 45% Bonds, 18% Equities, 35% Real Estate/Alternatives

GAC with the largest investors in Private Banking Magazine

LI in pandemic year with 5.6% return, less equities and more real estate / alternatives

DAX/MDAX: 5% return on plan assets of 340 billion euros

Savings banks and cooperative banks increase special funds volume by almost 12 billion euros

Pension funds for liberal professions: less than half fixed-income, one-third illiquid assets

GAC in dpn: The 100 largest investors in Germany

Pensionskassen with higher ratios for equities, real estates and alternatives

Savings banks with significantly increased real estate investments

Life insurance companies with very good performance 2019

GAC in dpn: DAX/MDAX - Pension obligations and assets at the all-time high

With God’s blessing – Church investors manage investments of over 100 billion euros

GAC in TiAM: Company Pension Funds and Pension Funds for Liberal Professions

GAC on the largest Depot A investors in dpn

GAC in dpn: The largest insurance companies in the DACH region

GAC in dpn: Asset Allocation fo pensions funds in Switzerland

GAC with update 2019 on asset allocation and performance of life insurance companies

GAC in IPE yearbook 2018: Equities- and real estates-exposure of 250 institutional investors

GAC with ranking of the largest institutional investors on

GAC discusses investments by churches in dpn-online

GAC appears in dpn-online discussing investments by social security funds

GAC with an update to pension funds of liberal professions (dpn)

GAC appears in IPE addressing the structure and performance of proprietary securities account (Depot A)

GAC in dpn: The 30 largest foundations in Germany

GAC discusses institutional investors in sweden

GAC discusses transition of the asset allocation (dpn)

GAC appears in the IPE yerabook addressing asset allocation and performance of corporates

GAC in Absolut Report: Asset Allocation and Performance of Company Pension Funds

GAC in Absolut Report: Asset Allocation and Performance of Pension Funds of Liberal Professions